Florida posted the worst foreclosure rate in the nation in May 2026 — one filing for every 2,110 housing units, against a national average of one in 3,562, according to ATTOM. Behind every one of those filings sits a months-long court process, and inside that process sits the most overlooked window in Florida real estate: the pre-foreclosure purchase. Learning how to buy a pre-foreclosure home in Florida means understanding that window — when it opens, when it slams shut, and the statutes that govern what you can and cannot do inside it. This guide walks the full path: finding the property, researching the debt, approaching the owner, structuring the deal, and closing before the auction.

What "Pre-Foreclosure" Actually Means in Florida

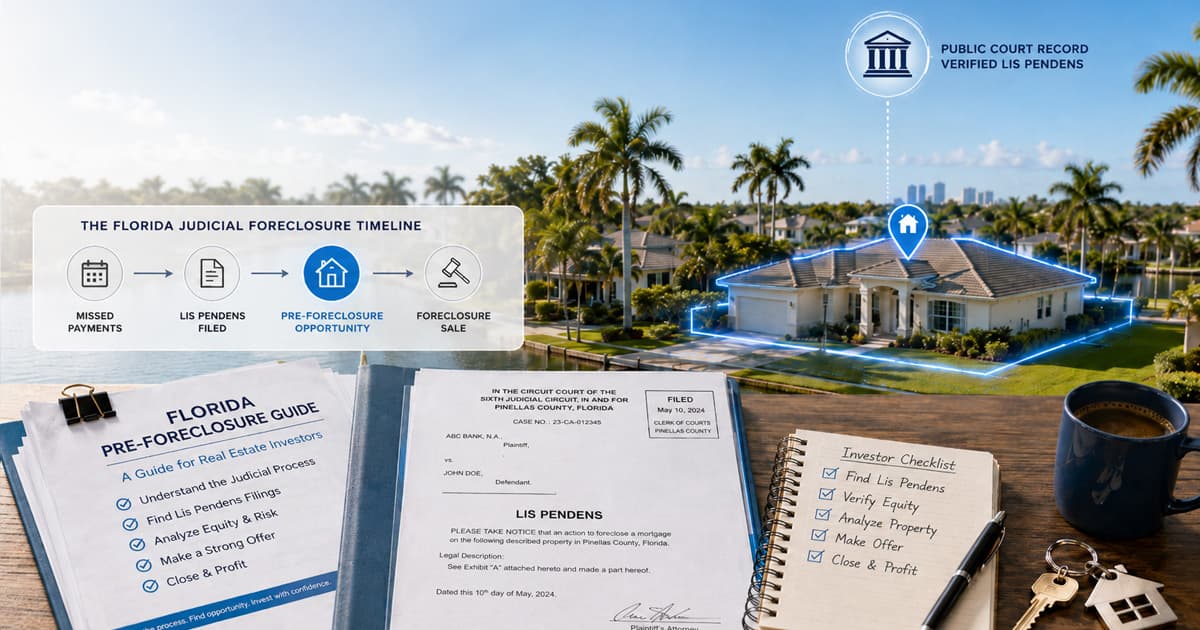

The Florida foreclosure process is judicial from start to finish. Florida Statute 702.01 puts it in six words: "All mortgages shall be foreclosed in equity." There is no out-of-court shortcut — a lender who wants to foreclose must file a lawsuit, and that lawsuit becomes public the moment a notice of lis pendens is recorded under F.S. 48.23. If you want the mechanics of that filing, read our deep guide to Florida lis pendens.

Pre-foreclosure is everything between that recorded notice and the courthouse auction. The critical fact: the homeowner still owns the property. You are not bidding against strangers on a clerk's website or buying sight-unseen from a bank. You are negotiating a private purchase with a person — one who is under a deadline. That is a completely different transaction from the auction itself, which comes with its own risks and its own pre-bid due-diligence checklist.

One legal consequence matters up front: once the lis pendens is recorded, anyone who acquires an interest in the property takes it subject to the outcome of that case (F.S. 48.23). Buying pre-foreclosure therefore means resolving the case at closing — paying the foreclosing creditor off so the suit is dismissed — not ignoring it.

The Florida Pre-Foreclosure Timeline — and Where Your Window Sits

ATTOM's Q1 2026 report found that properties foreclosed nationally in the first quarter had spent an average of 577 days in the foreclosure process. Florida's court-driven system is a big part of why distressed properties spend months — often longer — in limbo. Here is the sequence, and what each stage means for a buyer:

| Stage | Legal marker | What it means for a buyer |

|---|---|---|

| Lis pendens recorded | F.S. 48.23 | The case is public. Your window opens. |

| Litigation | F.S. 702.01 (foreclosure "in equity") | Months of court process. The owner can still sell to you at any point. |

| Final judgment | F.S. 45.031 | The court sets a public sale not less than 20 days or more than 35 days out. Your window is now measured in weeks. |

| Certificate of sale filed | F.S. 45.0315 | The owner's right to redeem — and your window — ends. |

| Certificate of title | F.S. 45.031 | If no objections are filed within 10 days, ownership passes to the auction's high bidder. |

Everything in this guide happens between the first row and the fourth.

Step 1: Find the Property Before the Auction Crowd Does

Every Florida pre-foreclosure starts as a court filing in the county where the property sits, so the raw material is public record: new foreclosure cases appearing on each county clerk's docket. The practical challenge is watching those dockets consistently and connecting each case to a property, an owner, and a mailing address — we covered the working options in how to find pre-foreclosure leads in Florida. A platform built for this, delivering Florida pre-foreclosure leads the day after they hit the docket, replaces that entire manual routine.

The volume is real. Across the four Florida counties PocketLeads currently covers — Collier, Lee County, Sarasota, and Pinellas — we indexed more than 1,000 new pre-foreclosure filings in roughly two months between May and early July 2026. Two details from that data set should reshape how you think about this market: roughly 1 in 5 of those properties had no mortgage recorded against them at all, and the median property carried a county-assessed market value of about $345,000. Foreclosure and equity coexist far more often than the stereotype of the underwater borrower suggests — and equity is exactly what makes a pre-auction purchase possible.

Step 2: Research the Debt, the Title, and the Numbers

Before you write an offer, read the case file. The docket tells you who is foreclosing, what they claim they are owed, and how far the case has progressed. Then verify three numbers:

The payoff. Florida law gives you a reliable tool here: under F.S. 701.04, once a written request is made by the owner — or by "any other person lawfully authorized to act on behalf of" the owner, which is why your contract should include that authorization — the mortgage servicer must send an estoppel letter with the payoff figure within 10 days.

Everything else on title. A voluntary sale wipes out nothing. Unlike an auction, where some junior interests can be extinguished by the judgment, a pre-foreclosure purchase transfers the property with every lien still attached — second mortgages, HOA claims, code liens, judgments. Order a title search early; every open item either gets paid at closing or becomes your problem.

The value. Run your own comparable sales and inspect the property if the owner allows it. The equity math is simple: market value, minus every payoff, minus your repair and closing costs. If that number is not meaningfully positive, the deal does not exist.

Step 3: Approach the Owner — and Know the Rules

The owner of a pre-foreclosure home is a person under court pressure, and Florida writes that fact directly into consumer-protection law. F.S. 501.1377 — aimed at "residential real property in foreclosure" — draws a sharp line between two kinds of deals.

A straightforward, arm's-length purchase — the owner sells, collects their equity at closing, and walks away with no strings attached — is an ordinary real estate transaction. That is the model this guide describes, and it is the model most wholesalers and investors should stick to.

A foreclosure-rescue transaction is different: the statute defines it as a deal where the property is conveyed but "the homeowner maintains a legal or equitable interest" — a lease-back, a repurchase option, a promise they can stay — and the deal is "designed or intended by the parties to stop, avoid, or delay foreclosure proceedings." Those deals are heavily regulated: the homeowner can cancel the agreement without penalty until 5 p.m. on the 3rd business day after signing, repurchase terms priced more than 17 percent per annum above what the buyer paid are presumptively unreasonable, and violations are unfair and deceptive trade practices carrying penalties up to $15,000 per violation.

The practical rules follow directly: put every offer in writing, never promise anyone they can "stay in the house" unless you intend to comply with the rescue-transaction rules, and give the owner room to seek advice. Respect is not just ethics here — it is what keeps a deal from unwinding.

Step 4: Structure the Deal — Full Payoff, Short Sale, or Walk Away

Every pre-foreclosure purchase resolves into one of three structures, and the estoppel letter from Step 2 tells you which one you are in.

The equity purchase. If your price covers every payoff with money left over, this is a standard purchase contract on a compressed clock. The owner nets the difference — often a far better outcome than letting the equity ride into an auction. For fix-and-flip investors, this is the cleanest acquisition channel in the distress market: direct negotiation, inspection access, and a conventional closing.

The short sale. If the property is worth less than the debt, the sale can only close if the lienholder releases its lien for less than full payoff. In a Florida short sale, the lender agrees in writing to accept the sale proceeds — and the terms of that approval letter matter enormously to the seller, because of what happens to the shortfall. Under F.S. 702.06, a deficiency judgment is "within the sound discretion of the court," and for an owner-occupied residence the deficiency "may not exceed the difference between the judgment amount, or in the case of a short sale, the outstanding debt, and the fair market value of the property on the date of sale." Sellers should push for an approval letter that waives the deficiency outright.

What about "subject-to"? You will hear investors pitch taking over the owner's existing loan. Understand the legal reality first: under the federal Garn-St Germain Act (12 U.S.C. § 1701j-3), a lender "may … enforce a contract containing a due-on-sale clause" — meaning a transfer without the lender's consent can make the entire balance immediately due. In an active foreclosure, where the lender is already accelerating the debt, that is not a loophole to build a deal on. Get title and legal advice before touching this structure.

And if none of the three works, walk away. The auction and the REO listing will still exist for properties whose numbers never made sense pre-auction.

Step 5: Close Before the Certificate of Sale

Florida gives the owner — and by extension, your deal — a hard statutory deadline. Under F.S. 45.0315, the mortgagor may cure the debt "at any time before the later of the filing of a certificate of sale by the clerk of the court or the time specified in the judgment." The statute's last sentence is the one to remember: "Otherwise, there is no right of redemption."

In practice that means a closing can happen even after final judgment — but once judgment is entered, the auction is set 20 to 35 days out, and your title company is now racing the clerk. Three habits keep the closing on the right side of that line: keep the estoppel letter current through your actual closing date, watch the case docket for the scheduled sale date, and have funds fully arranged before you go under contract. A pre-foreclosure deal that closes a week late is not a deal at all.

Frequently Asked Questions

Can you buy a pre-foreclosure directly from the owner in Florida?

Yes. Until the clerk files the certificate of sale, the homeowner owns the property and can sell it like any other seller. An arm's-length purchase where the owner keeps no interest in the property is an ordinary transaction; deals where the owner retains an interest or expects to stay are regulated foreclosure-rescue transactions under F.S. 501.1377.

How long does pre-foreclosure last in Florida?

Florida foreclosures run through the courts (F.S. 702.01), so there is no fixed length. Nationally, properties foreclosed in Q1 2026 had averaged 577 days in the process, per ATTOM. The window narrows sharply after final judgment, when the sale is set 20 to 35 days out under F.S. 45.031.

Can the owner still sell after the foreclosure judgment?

Yes. Florida's right of redemption (F.S. 45.0315) runs until the certificate of sale is filed or the time specified in the judgment, whichever is later — so a sale that pays off the judgment can close even after judgment is entered, right up until the auction result is docketed.

Do I need the lender's permission to buy a pre-foreclosure home?

Not if the sale pays the loan in full — you simply need an accurate payoff, which the servicer must provide within 10 days of a proper written request under F.S. 701.04. Lender approval is only required when the price cannot cover the debt and you need a short sale.

What happens to the foreclosure case when the purchase closes?

The closing funds pay the foreclosing creditor, the lien is satisfied, and the case is resolved — typically dismissed. Your title company will require the payoff and the case resolution as closing conditions, which is why the docket and the estoppel letter need to stay current through closing day.

Where do investors find pre-foreclosure homes in Florida?

Every case starts on a county clerk's docket, so you can monitor court records county by county — or use a platform that does it for you. PocketLeads delivers new pre-foreclosure filings from Florida county courts the day after they appear, matched to the property and owner.

Work the Window, Not the Courthouse Steps

The auction is the highest-competition, lowest-information moment in a Florida foreclosure. Everything before it favors the prepared buyer: direct negotiation, inspection access, verifiable payoffs, and a seller who benefits from the deal. The only hard part is being first — which is a data problem, not a talent problem.

PocketLeads delivers next-day pre-foreclosure leads for all four counties we currently cover — Collier, Lee, Sarasota, and Pinellas, with more Florida counties on the way — sourced from county court records and enriched with property and equity data. Start your free trial and see this week's filings before the auction crowd does.